The Indian government has officially launched the Emergency Credit Line Guarantee Scheme (ECLGS) 5.0 (ECLGS 5.0 Scheme), a strategic move to provide a financial safety net for Micro, Small, and Medium Enterprises (MSMEs). Approved by the Union Cabinet in May 2026, this version is specifically designed to help businesses navigate liquidity crunches caused by the ongoing West Asia conflict and rising operational costs.

For MSME owners, understanding the nuances of ECLGS 5.0 is critical to securing the working capital needed to sustain operations and protect jobs.

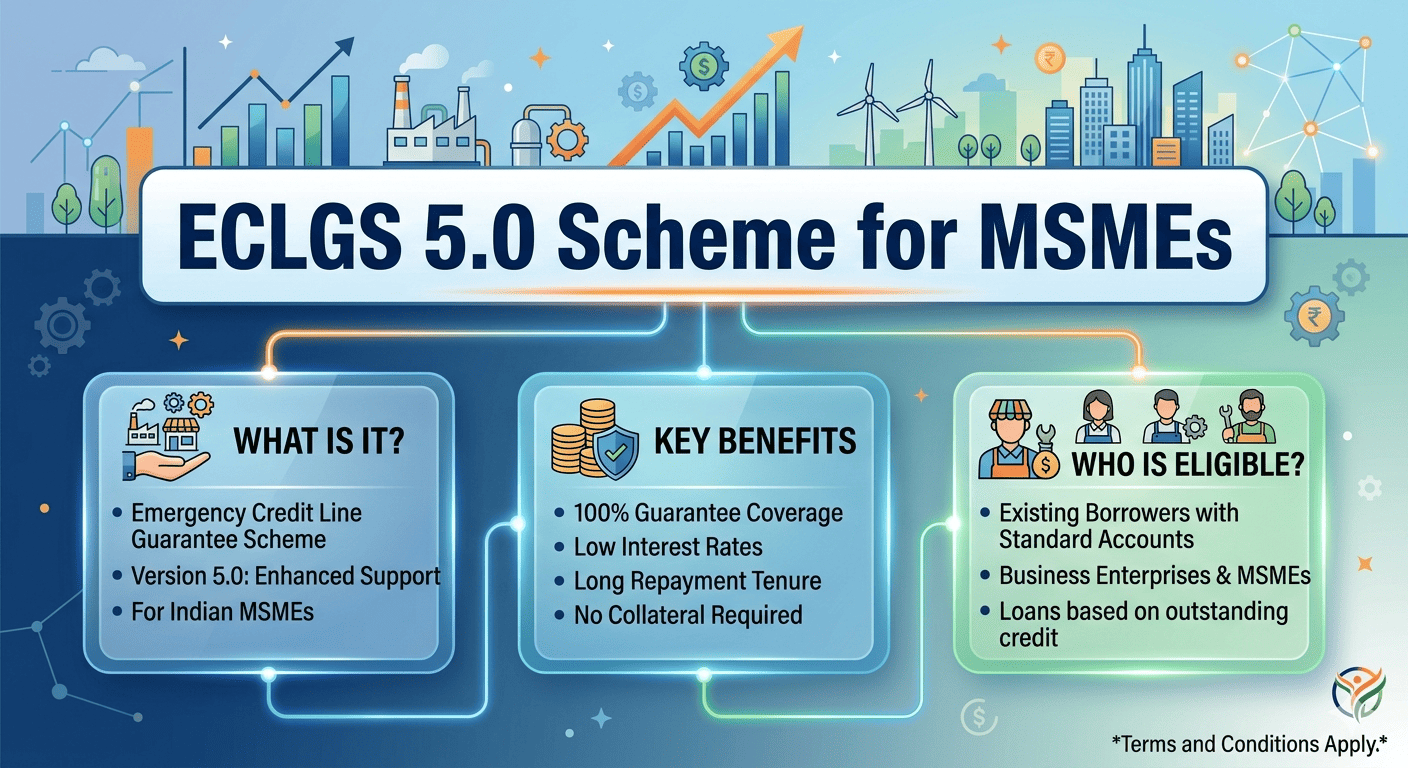

What is the ECLGS 5.0 Scheme?

ECLGS 5.0 is the latest iteration of the government’s flagship credit guarantee program. Administered by the National Credit Guarantee Trustee Company (NCGTC), it facilitates additional credit flow to businesses without requiring extra collateral.

The scheme targets a total additional credit flow of ₹2.55 lakh crore, ensuring that the “backbone of the Indian economy”—the MSME sector—remains resilient against global supply chain disruptions.

Key Highlights for MSMEs:

- 100% Sovereign Guarantee: For MSMEs, the government provides a full 100% guarantee on the additional credit, reducing the risk for banks and making loan approval faster.

- Zero Guarantee Fee: Borrowers are not required to pay any additional fee to avail of this guarantee.

- Interest Rate Caps: Interest rates are regulated to ensure affordability, typically capped at 9% for banks and 13% for NBFCs.

Eligibility Criteria for MSMEs

To benefit from ECLGS 5.0, your business must meet specific requirements as of March 31, 2026:

- Account Status: Your existing credit facilities must be classified as “Standard” (not a Non-Performing Asset or NPA).

- Existing Borrowers: Only businesses with existing working capital limits or term loans are eligible.

- Registration: While not always mandatory for the loan, having a valid Udyam Registration is highly recommended to streamline the process.

Financial Support and Repayment Terms of ECLGS 5.0 Scheme

The scheme offers a structured approach to borrowing that prioritizes business stability over immediate repayment.

Quantum of Support

MSMEs can avail of additional credit up to 20% of their peak working capital utilized during the fourth quarter (Q4) of FY 2025-26. This additional funding is capped at ₹100 crore for non-airline borrowers.

Repayment Structure

The loan is designed to give businesses “breathing room”:

- Tenure: 5 years from the date of the first disbursement.

- Moratorium: A 1-year moratorium on the principal amount, meaning you only pay interest during the first 12 months.

- Interest Conversion: A unique feature allows businesses to convert up to 50% of the interest due into a Funded Interest Term Loan (FITL), significantly easing immediate cash flow pressure.

How to Apply for ECLGS 5.0 Scheme

MSMEs do not need to hunt for new lenders. The scheme is implemented through your existing Member Lending Institutions (MLIs)—the banks or NBFCs where you already hold a credit account.

- Check with your Bank: Reach out to your relationship manager to confirm your “Standard” account status.

- Calculate Limit: Determine 20% of your peak utilization from Jan–March 2026.

- Documentation: Provide updated GST returns, bank statements, and your Udyam Certificate.

- Sanction & Disbursement: Once the MLI approves, the NCGTC issues the guarantee, and funds are disbursed directly to your account.

Note: The scheme is valid for loans sanctioned until March 31, 2027, or until the ₹2.55 lakh crore limit is reached.

Why ECLGS 5.0 is a Game Changer for MSMEs

According to recent reports, earlier versions of ECLGS saved over 13.5 lakh MSME accounts from turning into NPAs and protected nearly 1.5 crore jobs.

With the West Asia crisis impacting fuel prices and international trade routes, ECLGS 5.0 acts as a bridge. It allows MSMEs to:

- Maintain Liquidity: Pay suppliers and staff on time despite payment delays.

- Avoid Collateral Stress: Access funds without pledging additional property or assets.

- Scale Operations: Use the extra capital to pivot or adapt to changing market conditions.

By leveraging this government-backed support, MSMEs can transform a period of global uncertainty into an opportunity for internal strengthening and long-term resilience.