For a Micro, Small, or Medium Enterprise (MSME) in the manufacturing sector, managing upfront costs is often the biggest hurdle to growth. Recognizing this, the Central Board of Indirect Taxes and Customs (CBIC) has introduced a game-changing category: the Eligible Manufacturer Importer (EMI) under Eligible Manufacturer Importer Scheme (EMI Scheme)

Announced in the Union Budget 2026-27, this scheme is specifically designed to ease the financial burden on compliant manufacturers who rely on imported raw materials or capital goods.

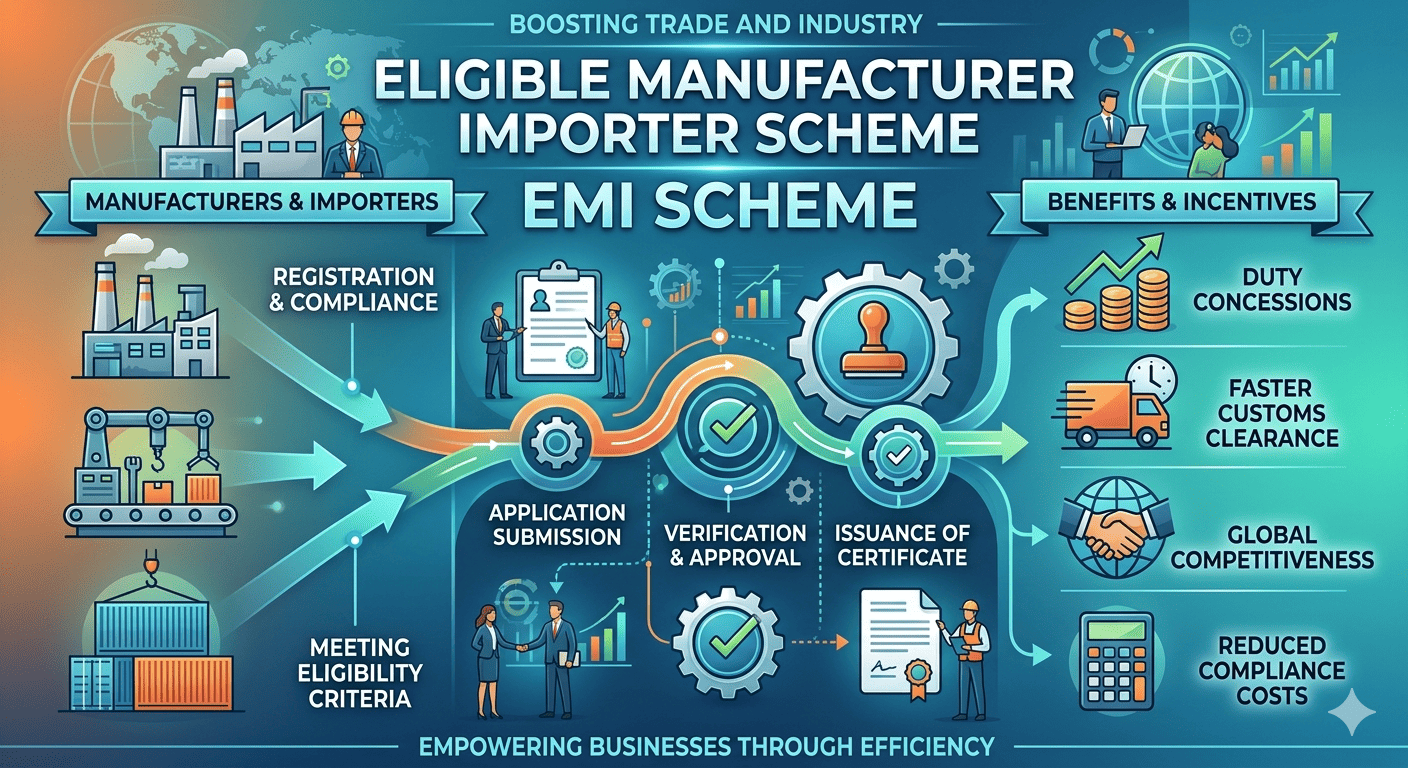

What is an Eligible Manufacturer Importer Scheme (EMI Scheme)?

An Eligible Manufacturer Importer is a trusted business category that allows manufacturers to clear imported goods at ports without paying customs duty at the time of clearance. Instead of an immediate cash outflow, the EMI status enables deferred payment, allowing the business to settle its customs dues on a monthly basis.

Key Timeline: The EMI facility is operational from April 1, 2026, until March 31, 2028.

Why the EMI Status is a Game-Changer for MSMEs

The primary goal of the EMI scheme is to move from a “transaction-based” system to a “trust-based” system. For MSMEs, this translates into three major advantages:

- Enhanced Working Capital: You no longer need to lock up your cash in customs duties while your goods are still in transit or sitting in a warehouse.

- Faster Port Clearances: Goods are cleared immediately upon filing the Bill of Entry without waiting for duty payment confirmation, reducing demurrage charges.

- Path to AEO Certification: The EMI scheme acts as a bridge, encouraging MSMEs to eventually attain Authorised Economic Operator (AEO) T2 or T3 status, which offers even higher levels of global trade facilitation.

Eligibility Criteria for MSMEs (Eligible Manufacturer Importer Scheme)

To qualify as an EMI, your MSME must meet specific benchmarks defined by the CBIC under Circular No. 08/2026-Customs:

- Manufacturer Status: You must be a manufacturer as defined under Section 2(72) of the CGST Act or send goods to a job worker under Section 143 of the Act.

- Compliance Record: A clean track record with Customs and GST is mandatory. This includes no history of arrests or convictions for the directors or partners.

- AEO-T1 Advantage: Existing AEO-T1 certified entities (including MSMEs) are fast-tracked for eligibility, provided they meet the basic compliance criteria.

- Financial Standing: MSMEs must demonstrate a stable financial record and a minimum turnover as prescribed in the operational guidelines.

How the Deferred Payment Works

Under the Deferred Payment of Import Duty Rules, 2016, the payment schedule for an EMI is streamlined:

| Period of Import | Duty Payment Deadline |

| Goods cleared between 1st – 31st (April to Feb) | By the 1st of the following month |

| Goods cleared in March (1st – 31st) | By March 31st (same month) |

Steps to Apply for EMI Status

The application process is fully digital and transparent. Follow these steps to register:

- Visit the Portal: Go to the official AEO India website at www.aeoindia.gov.in.

- Locate the EMI Tab: Select the “Eligible Manufacturer Importer” tab.

- Submit Documentation: Upload your valid Importer-Exporter Code (IEC), MSME Udyam Registration, and GST compliance history.

- Verification: The Directorate of International Customs (DIC) will review the application. Once approved, your status is automatically updated in the Customs Automated System (ICEGATE).

MSME Bytes Thoughts for Small Business Owners

The EMI scheme is a clear signal that the government is committed to the “Make in India” initiative by supporting the backbone of the economy—MSMEs. By deferring duty payments, your business can reinvest that saved capital into production, labor, and scaling operations.